Promotion of Accounting Reform as the most effective Pathway to a Fairer Safer and more Prosperous Society. Comment and Support from all quarters is Sought to straighten out NZ's problem

To Contact Us to page back through Previous Editions click here Index is in right hand column>May 2009 Edition ----Right, we start this month with a protest at the appointment of Joan Withers to the Board of Mighty River Power.

Mighty River power is an electricity SOE which we understand controls the electricity stations on the Waikato river among others. The SOE minister is Mr Simon Power who is also Minister of Commerce and Justice. Mr Power we think is somewhat famous for sort of paraphrasing prime minister Michael Savage with an “Where the USA, Britain and Australia . goes we go” statement in May 2004 that got him downgraded in the Don Brash hierarchy. He has reviewed and made changes to the composition of most SOEs and the Commerce Commission but is yet to touch the Securities Commission which we say should have been the first one to he operated upon. His appointment of Ms Withers to Mighty River gives us the impression that he is under the power of Credit Suisse and associates and is not prepared to assist Feltex Shareholders to get their money back. We should not be alone in this protest. The Shareholders Assn has called for the Feltex IPO directors not to be allowed to be a director of anything for 5 years. This appointment is just not good enough. . Another association we have just realized is that Securities Commission member John Holland is a senior partner of the legal firm Chapman Tripp which is representing several former Feltex Carpets directors with respect to actions being taken against them. Another Securities Commission member David Jackson was of course an Auckland audit partner of the firm that audited the Auckland based Feltex Carpets at the time of its IPO. He and Elizabeth Hickey are both ex Ernst and Young accountants on the commission. That history alone should disqualify them from being there. Ms Withers became a director of Feltex Carpets Ltd, we understand some 10 days before that company issued a prospectus offering all its share capital in an IPO in April 2004. She allowed her name and photo to go in the prospectus declaring her a director of the company. She “resigned” from the board barely a year later, we understand after the company made an announcement significantly reducing its forecasted profit for its 2005 year from that projected in the prospectus. We contend that: a: Ms Withers had a duty to study the company thoroughly before accepting an invitation to join the Feltex board, including the intended prospectus. We contend that any reasonable study of that prospectus would have concluded that it was fraudulent. Practically all institutions knew to leave the issue alone the exception being the ACC whose then investment chairman Mr (soon to be Sir apparently) Eion Edgar also headed one of the two lead brokers for the issue, Forsyth Barr, He needs to be stripped of his honour. b As she was a new director subscribers to Feltex had reason to believe that she would be there for far longer than one year barring death or ill health, which have not been factors. Resigning and getting out is not an option for a responsible director when trouble arises in a company. And directorships can not be used as a fill in between employment spells unless this was clearly explained to potential shareholders from the beginning. We submit that the employment offer from Fairfax was just a jackup to get her out. David Kirk who appointed her is now working for Forsyth Barr which we suspect was part of the deal. She remained on the Auckland Airport board. It was running smoothly. If the job could accommodate one only directorship on the side she should have chosen Feltex because it most needed competent and honest directors and presumably she claimed to be one. You do not want directors on Mighty River Power or anywhere else that will pack up and leave should the going get tough. We do not know what her parting message to Feltex shareholders would have been. We can only surmise it would be something like this. “I have been fortunate to have been offered a good opportunity to further my employment career in the news media. I can only keep one directorship on with this job and Auckland Airport would seem to be a better long term prospect. You are therefore losing a director who has grips on the current troubles facing Feltex and has been working hard to try to resolve them. Stiff cheese but my interests come first. Joan”. Ms Withers should have been aware that her female status possibly attracted many of the “Mum and Dad” investors which apparently constitute most of the Feltex shareholding and she thus had a clear duty to fight for them right to the end. The liquidators of Feltex are pursing action against certain directors for mismanagement following Ms Withers departure, claiming considerable losses were unjustified. This would counter any argument that Feltex shares were effectively worthless when Ms Withers left. As evidence of the fraudulent nature of the Feltex IPO we cite the critical assumptions upon which projections of revenue income for the 2005 year were made. They were a 1% p.a. increase in revenue due to increased market share and a 1% increase in market size. The prospectus did not contain any specific information on how the company was faring with respect to market share but it could be calculated that it was losing share at the rate of 5% p.a. for the past two years. The difference between a 2% rise and a 10% drop between 2003 and 2005 is colossal. Percentage loss of income tends to be several times that of lost of revenue.

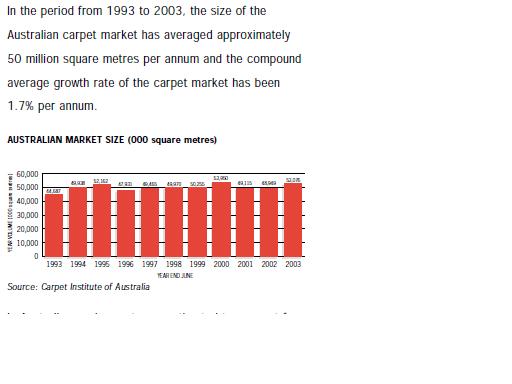

With regard to the misrepresentation of market size we refer you to page 37 of the prospectus where it has a graph of market size for the Australian market. Our interest in the affair is in getting justice for Feltex shareholders who we believe were swindled of their fund by statements made in the IPO prospectus. Many people like Ms Withers, involved with the IPO, either did not do their homework or just went along with it. By appointing her to Mighty River you are giving credibility to the IPO without justification. While we still think the Securities Commission played a large part in getting Ms Withers into Feltex and getting her out again we now believe Ms Withers still maintains close ties with Credit Suisse and associates. They were paid about $6m by Auckland Airport for efforts in warding off the partial takeover offer for the Airport company by a “top shelf” overseas institution. The very late timing of a rejection of the offer by ministers is most peculiar. Ms Withers probably stood to lose her directorship of the Airport company if the buy-in had been successful. . Ms Withers became a director of Feltex Carpets Ltd, we understand some 10 days before that company issued a prospectus offering all its share capital in an IPO in April 2004. She allowed her name and photo to go in the prospectus declaring her a director of the company. She “resigned” from the board barely a year later, we understand after the company made an announcement significantly reducing its forecasted profit for its 2005 year from that projected in the prospectus. We contend that: a: Ms Withers had a duty to study the company thoroughly before accepting an invitation to join the Feltex board, including the intended prospectus. I contend that any reasonable study of that prospectus would have concluded that it was fraudulent. Practically all institutions knew to leave the issue alone the exception being the ACC whose then investment chairman Mr (soon to be Sir apparently) Eion Edgar also headed one of the two lead brokers for the issue, Forsyth Barr, He needs to be stripped of his honour. b As she was a new director subscribers to Feltex had reason to believe that she would be there for far longer than one year barring death or ill health, which have not been factors. Resigning and getting out is not an option for a responsible director when trouble arises in a company. And directorships can not be used as a fill in between employment spells unless this was clearly explained to potential shareholders from the beginning. We submit that the employment offer from Fairfax was just a jackup to get her out. David Kirk who appointed her is now working for Forsyth Barr which we suspect was part of the deal. She remained on the Auckland Airport board. It was running smoothly. If the job could accommodate one only directorship on the side she should have chosen Feltex because it most needed competent and honest directors and presumably she claimed to be one. You do not want directors on Mighty River Power or anywhere else that will pack up and leave should the going get tough. We do not know what her parting message to Feltex shareholders would have been. We can only surmise it would be something like this. “I have been fortunate to have been offered a good opportunity to further my employment career in the news media. I can only keep one directorship on with this job and Auckland Airport would seem to be a better long term prospect. You are therefore losing a director who has grips on the current troubles facing Feltex and has been working hard to try to resolve them. Stiff cheese but my interests come first. Joan”. Ms Withers should have been aware that her female status possibly attracted many of the “Mum and Dad” investors which apparently constitute most of the Feltex shareholding and she thus had a clear duty to fight for them right to the end. The liquidators of Feltex are pursing action against certain directors for mismanagement following Ms Withers departure, claiming considerable losses were unjustified. This would counter any argument that Feltex shares were effectively worthless when Ms Withers left. As evidence of the fraudulent nature of the Feltex IPO we cite the critical assumptions upon which projections of revenue income for the 2005 year were made. They were a 1% p.a. increase in revenue due to increased market share and a 1% increase in market size. The prospectus did not contain any specific information on how the company was faring with respect to market share but it could be calculated that it was losing share at the rate of 5% p.a. for the past two years. The difference between a 2% rise and a 10% drop between 2003 and 2005 is colossal. Percentage loss of income tends to be several times that of lost of revenue. With regard to the misrepresentation of market size I refer you to page 37 of the prospectus where it has a graph of market size for the Australian market. The sentence above the graph stated that in the period 1993 to 2003 (as covered by the graph) the compound average growth rate was 1.7% p.a.. It is true that if you apply 1.7% compound growth for 10 years to the 1993 figure you get the 2003 figure but it is quite fraudulent to imply that this has relevance to the growth of the market. The 1993 figure is very low. It is the lowest at least since 1989. The 1990 figure was amongst the highest. The 2003 figure is the second highest of these years. If you use least squares regression analysis on the years 1994 to 2003 (an objective number of 10 years) you get compounding growth of some 0.38% p.a.. More importantly it shows the 2003 figure to be close to 2% above the average line. Because it is likely that some individual years will fall as far below the average line as others go above it, it can be argued that a 4% drop in revenue from that of 2003 should be allowed for in predicting market size in 2005, not a 1 or 2% increase they say they have used. Proper use of market size and market share trend extensions would probably have predicted the 2005 profit quite accurately. Import protection for manufacturers such as Feltex was of course being reduced in both countries. That was the likely reason for Shaw Industries selling its Melbourne manufacturing plant (to Feltex) in 2000. Probably Shaws gave Feltex some leeway before it started actively competing as an importer but whether this is so is not mentioned in the prospectus as far as we know. Our interest in the affair is in getting justice for Feltex shareholders who we believe were swindled of their funds by statements made in the IPO prospectus. Many people like Ms Withers, involved with the IPO, either did not do their homework or just went along with it. By appointing her to Mighty River the minister is giving credibility to the IPO without justification.. While we still think the Securities Commission played a large part in getting Ms Withers into Feltex and getting her out again we now believe Ms Withers still maintains close ties with Credit Suisse and associates. They were paid about $6m by Auckland Airport for efforts in warding off the partial takeover offer for the Airport company by a “top shelf” overseas institution. The very late timing of a rejection of the offer by ministers is most peculiar. Ms Withers probably stood to lose her directorship of the Airport company if the buy-in had been successful. |

Ms Withers is not an accountant and does not claim to be one as far as we know. She has an MBA apparently. But she hits the headlines on this site because her involvement with Feltex Carpets Ltd (now Exftx Ltd in liquidation) seems to be stopping accounting scandals involving that company’s Initial Public Offering in 2004 from being judicially resolved. Both the country’s most highly honoured accountant of the decade the Institute of Chartered Accountants Accounting Supremo of the decade are up to their necks in aspects of the Feltex affair and theirs is but small pieces of the scandal.

Ms Withers is not an accountant and does not claim to be one as far as we know. She has an MBA apparently. But she hits the headlines on this site because her involvement with Feltex Carpets Ltd (now Exftx Ltd in liquidation) seems to be stopping accounting scandals involving that company’s Initial Public Offering in 2004 from being judicially resolved. Both the country’s most highly honoured accountant of the decade the Institute of Chartered Accountants Accounting Supremo of the decade are up to their necks in aspects of the Feltex affair and theirs is but small pieces of the scandal.  The sentence above the graph stated that in the period 1993 to 2003 (as covered by the graph) the compound average growth rate was 1.7% p.a.. It is true that if you apply 1.7% compound growth for 10 years to the 1993 figure you get the 2003 figure but it is quite fraudulent to imply that this has relevance to the growth of the market. The 1993 figure is very low. It is the lowest at least since 1989. The 1990 figure was amongst the highest. The 2003 figure is the second highest of these years. If you use least squares regression analysis on the years 1994 to 2003 (an objective number of 10 years) you get compounding growth of some 0.38% p.a.. More importantly it shows the 2003 figure to be close to 2% above the average line. Because it is likely that some individual years will fall as far below the average line as others go above it, it can be argued that a 4% drop in revenue from that of 2003 should be allowed for in predicting market size in 2005, not a 1 or 2% increase they say they have used. Proper use of market size and market share trend extensions would probably have predicted the 2005 profit quite accurately. Import protection for manufacturers such as Feltex was of course being reduced in both countries. That was the likely reason for Shaw Industries selling its Melbourne manufacturing plant (to Feltex) in 2000. Probably Shaws gave Feltex some leeway before it started actively competing as an importer but whether this is so is not mentioned in the prospectus as far as we know.

The sentence above the graph stated that in the period 1993 to 2003 (as covered by the graph) the compound average growth rate was 1.7% p.a.. It is true that if you apply 1.7% compound growth for 10 years to the 1993 figure you get the 2003 figure but it is quite fraudulent to imply that this has relevance to the growth of the market. The 1993 figure is very low. It is the lowest at least since 1989. The 1990 figure was amongst the highest. The 2003 figure is the second highest of these years. If you use least squares regression analysis on the years 1994 to 2003 (an objective number of 10 years) you get compounding growth of some 0.38% p.a.. More importantly it shows the 2003 figure to be close to 2% above the average line. Because it is likely that some individual years will fall as far below the average line as others go above it, it can be argued that a 4% drop in revenue from that of 2003 should be allowed for in predicting market size in 2005, not a 1 or 2% increase they say they have used. Proper use of market size and market share trend extensions would probably have predicted the 2005 profit quite accurately. Import protection for manufacturers such as Feltex was of course being reduced in both countries. That was the likely reason for Shaw Industries selling its Melbourne manufacturing plant (to Feltex) in 2000. Probably Shaws gave Feltex some leeway before it started actively competing as an importer but whether this is so is not mentioned in the prospectus as far as we know. Advertising section

We link to: Accounting Page - Comprehensive Accounting Resources and Directory.Internet Web Directory - The internet's fastest growing directory of the best web sites. Fully searchable and updated regularly. We Advertise:

Books

Case studies of ICANZ coverups 2 Ernst and Young report to Dairy Co shareholders

Pokemon

Gifts

Cars

Toys

MP3

Videos

Dolls

Garden tools

Jewelry

------------------------

Structure and Operation of an alternative Accounting Organisation designed to shun dishonesty.

Suitable Objectives

Register of Members

Members Forum - Topical * open to all meantime: Plenty of Opinion

Magazine Plans

Need an Accountant? or Prepared to Change?

Users Forum * have your say

Ready to Join?Offering some Help?

Knowledge Tests * being developedInformation Bulletins

Why it is being Proposed

What's Wrong with the existing accounting body?

So called BNZ Auditan extensive case study Current Attitudes of Existing Institute

Visit our Advertising page from

Here