To Contact Us to page back through Previous Editions click here Index is in right hand column

June 2009 Edition ----

We think about now we have completed 10 years service in exposing scandal in the new Zealand accounting scene. Things have not got any better though in fact we think they have got worse. We need people to join us to get things under control.

This month we wish to complain about the title of “Sir” which we believe is about to be conferred upon a Fellow and at the same time an Associate of the Institute of Chartered Accountants of NZ, one Eion Edgar.

Mr Edgar, hopefully we have got in before the conferring and can call him that although even “Mr” is stetching things rather too much, is in our vry bad books for his unjustified support of the Initial Public Offer of Exftx ltd – in receivership and Liquidation (then known as Feltex Carpets Ltd) in May 2004.

As we understand it Mr Edgar was chairman of directors of the sharebroking firm Forsyth Barr at the time of this IPO and Forsyth Barr was one of the two “Lead Brokers” for the issue. The other Lead broker, First NZ Capital has historic connections with the global firm Credit Suisse which would appear to have close connections with the promoters of the issue and with the vendors of the issue by virtue of them all having the words “Credit Suisse” in their name. Hence Mr Edgar should have been well aware that the other joint broker probably had a vested interest in the issue. The prospectus implies that the lead brokers participated in the planning of the offer. Mr Edgar was also a director of the Accident Compensation Corporation at the time of the issue and the chairman of its Investment Committee. As we understand it the ACC was virtually the only institution to subscribe to the issue and it did so to the extent of some $9m.

We contend that as chairman of the independent lead broking firm Mr Edgar had a clear duty to check out the validity of the Feltex offer as presented by the prospectus and this he has either failed to do or he has ignored his findings. We claim that within the prospectus itself there was ample evidence that this was a fraudulent offer. We claim that he had a duty to check it out before the offer opened and even if he failed to do this he had a duty to check it out and call the offer off when he discovered that institutions were not taking up the offer. We believe that he knew full well from the start that the offer was a have but chose to go along with the lucrative venture which targeted a vulnerable investor class.

A forecast of the 2004 Feltex profit and a projection of the 2005 profit and resulting dividends featured highly in the message of the prospectus. The 2005 projections were primarily based upon assumptions of a one percent increase in market size and a one percent increase in market share (which we have interpreted as being a one percent increase in revenue due to increased market share) over the previous year.

We claim that Mr Edgar had reason to be suspicious about the magnitude of the offer because of falling tariff protection for the rather labour intensive industry in both Australia and New Zealand, that Shaw Industries had got out of carpet manufacture in Australia, attractive brokerage fees were being offered, and the then sole owner of Feltex intended exiting the company completely.

We submit that Mr Edgar had a duty to examine Feltex’s recent experience with respect to market growth and market share and to compare this with the 1% p. a. allowed for each of market growth and increased market share in the revenue and income projections for the company’s 2005 year. We submit that Mr Edgar should have been concerned to find that the prospectus did not directly set out Feltex’s recent history of market share. When this is calculated from other information given it can be seen that it was falling at the rate of 9% and 7% for each of the latest two years for which data was available.

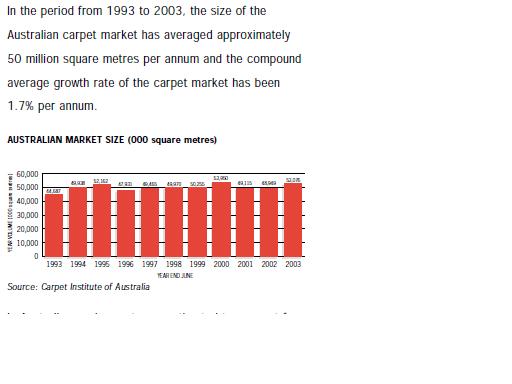

It should have also been obvious to him that the prospectus at page 37 had fraudulently inferred that the Australian carpet market size had grown at an average compound rate of 1.7% p.a. over the latest 10 year period of available figures. We here present the relevant section of the prospectus being part of page 37.

The sentence above the graph stated that in the period 1993 to 2003 (as covered by the graph) the compound average growth rate was 1.7% p.a.. It is true that if you apply 1.7% compound growth for 10 years to the 1993 figure you get the 2003 figure but it is quite fraudulent to imply that this has relevance to the growth of the market. The 1993 figure is very low. It is the lowest at least since 1989. The 1990 figure was amongst the highest. The 2003 figure is the second highest of these years. It is not rational to use the figures for just two years to calculate the recent trend, especially when one of them is eleven years ago and barely relevant. Least squares regression analysis is able to take the figures for all the most relevant years into account.

If you use least squares regression analysis on the years 1994 to 2003 (an objective number of 10 years) you get compounding growth of some 0.3% p.a.. More importantly it shows the 2003 figure to be close to 2% above the average line. Because it is likely that some individual years will fall as far below the average line as others go above it, it can be argued that a 4% drop in revenue from that of 2003 should be allowed for in predicting market size in 2005, not a 1 or 2% increase they say they have used.

Proper use of market size and market share trend extensions would probably have predicted the 2005 profit quite accurately. There was no scope for market yield dividends on $250m. Perhaps $10m or $20m could have been supported.

We submit that the above information which was readily available to Mr Edgar should have made it clear to him that the likelihood was that disaster awaited Feltex and he should not have had anything to do with the offer and he should have warned potential investors against it.

The Securities Commission issued a one page news release on 25 August 2006 saying that it had completed an investigation into the Feltex IPO prospectus and found no breaches of securities law. It said that no further action would be taken in respect to the matter. It defied this latter assertion however on 11 October 2007 when it issued a report on Feltex’s IPO Prospectus, Financial Reporting and Continuous Disclosure. The Companies office has brought charges against the accounting institute’s most recently appointed life member, probably as a result of this report being referred to it at paragraph 208. Also, at paragraphs 209 and 210 it refers to the Institute its conclusion that the work of auditor Gordon Fulton failed to meet required standards.

Part IV of the report is 2 ˝ pages long and is devoted to further consideration of the IPO although none of its conclusions were changed. In paragraph 61(a) contained in part IV the Commission states the critical assumption that “the carpet market in Australia and New Zealand would continue to grow by 1% (total market sales), which is stated to be below the average growth rate of the past 10 years”. That is roughly what the prospectus officially says about the 1% growth assumption but it would be clear to the Commission that this growth assumption is untrue. However despite this the Commission has decided to endorse it. Our calculations for the growth of the carpet markets for the ten years 1994 to 2003 using least squares regression analysis, available from here is 0.31% p.a. compounding, for the Australian market, 1.7% for the New Zealand market and 0.45% for the two markets combined. More importantly it shows the 2003 combined market size to be some 4.34% above the average line. On the assumption that actual market size will go as much below the average line as it goes above it, we submit that Feltex’s 2003 sales should have been multiplied by 0.967 to make a fair adjustment for market size influences based upon recent history not the 1.01 or 1.02 that they will have used. This is not a pessimistic outlook. Actual figures will of necessity go below an average line as much as the go below it and 2005 was almost a sure bet for a low point.

No market size figures in terms of total dollar sales are quoted the prospectus. Feltex has chosen to present market size information in terms of square meters of carpet, and not of carpet sold, but carpet supplied to the market, so that so that increases in or depletion of stocks are not taken into account. I would expect that these were the only figures on market size that were available or the were considered to be the best ones for consideration of market size. I claim that it would be completely improper to for Feltex to present market size information to investors in terms of square meters supplied to the market and justify their 1% market growth assumption to the Securities Commission in terms of total market sales data and I don’t believe that it has done so. We claim that the Commission is simply spinning a story in its paragraph 61(a) and it is not at all interested in establishing what actually went on. It has decided to declare that all actions of Feltex prior to its profit downgrade announcement in early 2005 and the resignation of Joan Withers as a director were above board for its own purposes which we speculate about below.

We now wish to consider the issue of market share. Our calculations which we set out in the same document show that Feltex’s market share dropped from $5.90 per square meter of total carpet supplied to its Australasian market in its 2001 year to $5.32 in 2002 to $4.93 in 2003. The figures are in 2003 dollars. This represents falls of 9.95% and 7.26% respectively between years. The effect of falling tariff protection and competition from Shaws, the former owner of Feltex’s Australian plant was showing. Feltex was unrealistically projecting a turnaround to at least a 1% increase in 2005.

Paragraph 61 of the Securities Commission’s report says that the Commission found that most of Feltex’s assumptions presented a largely “no change” scenario. We challenge this statement absolutely and say the assumptions represent dramatic upturns from the established pattern.

Mr Edgar became chairman of the NZ Olympic Committee in 2003, about the same time as he joined the ACC board. We speculate that the Securities Commission’s refusal to acknowledge that there was anything wrong with the Feltex IPO was because it was a raid on the unsuspecting populous to pay for a few gold and silver medals for NZ athletes at the 2004 Olympic games with cross party political support.. The NZ winners there put in phenomenal performances, especially those with a cycling component. The sport of cycling was widely believed to be rife with performance enhancing drug taking at the time.

As stated above we understand Mr Edgar is about to become Sir Eion Edgar. New Zealand is alone in reverting back to these ancient titles. I believe the motive is to give certain people extra protection from criminal or similar investigation and I trust that your institute will not be influenced by this age old trick.

to top of pageAdvertising section

We link to: Accounting Page - Comprehensive Accounting Resources and Directory.Internet Web Directory - The internet's fastest growing directory of the best web sites. Fully searchable and updated regularly. We Advertise:

Books

Case studies of ICANZ coverups 2 Ernst and Young report to Dairy Co shareholders

Pokemon

Gifts

Cars

Toys

MP3

Videos

Dolls

Garden tools

Jewelry

------------------------

Structure and Operation of an alternative Accounting Organisation designed to shun dishonesty.

Suitable Objectives

Register of Members

Members Forum - Topical * open to all meantime: Plenty of Opinion

Magazine Plans

Need an Accountant? or Prepared to Change?

Users Forum * have your say

Ready to Join?Offering some Help?

Knowledge Tests * being developedInformation Bulletins

Why it is being Proposed

What's Wrong with the existing accounting body?

So called BNZ Auditan extensive case study Current Attitudes of Existing Institute

Visit our Advertising page from

Here