To Contact Us

to page back through Previous Editions click here Index is in right hand column

July 2009 Edition ----

Well we don’t really want to give up the topic of the Feltex IPO. We say the practice of selecting an earlier low point and a recent high point, drawing a line through them and assuming the slope of the line to represent the growth of whatever is being considered is absolutely disgusting. If such a growth measurement is used to forecast or project future growth for the purpose of selling a business that is corruption. And if inspecting authorities fail to recognize it as corruption then that is corruption also.

We are referring to the 2004 Feltex IPO and the prospectus issued with respect to this offer. The prospectus supplies a projection of the company’s income for its 2005 year and uses the results of this projection to suggest what income the subscribers could expect by way of dividend. Critical assumptions used in calculating the projection were, market share rising at the rate of 1% p.a. from that of the last known record of market size, being the year to June 2003, and the companies market share increasing by an amount equivalent to 1% of previous year’s sales. .

Despite giving the impression of providing extensive financial information the prospectus did not show the company’s recent experience with respect to market share although with a little effort it could be calculated to be falling from approximately $5.90 per square meter of total carpet supplied to its Australasian market in its 2001 year to $5.32 in 2002 to $4.93 in 2003. These are falls of approximately 9% and 7% respectively.

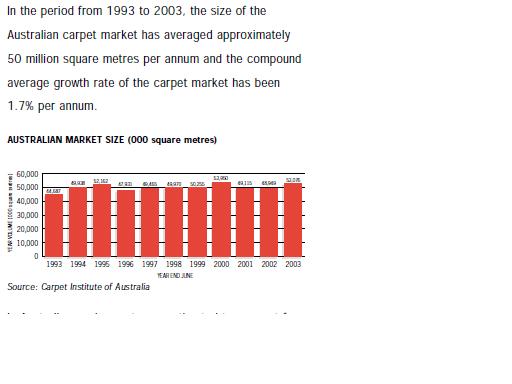

With respect to market size we repeat again the section of the prospectus at page 37 shows graphs of this statistic for the years 1993 to 2003 and says that the Australian market has grown by 1.7% p.a. compounding between these years.

We follow this up with a line graph showing the years 1990 to 2005 on the x axis and carprt quantity on the y axis. The first 40 million sq meters is not shown so the differences between years is exaggerated on the graph.

The series 1 line shows the same figures as the page 37 bar graph but with the years 1990 to 1992 added. Series 2 is the 1.7% compounding growth line derived by Feltex. This calculation takes only these two years into account. As can be seen 1993 was a very low year in terms of market size growth and 2003 was a high one. Series 3 is a projection of that same line from 2003 and Series 4 is the 1% compound growth line as apparently was used by Feltex for their projection of the company’s 2005 revenue.

With respect to market size we repeat again the section of the prospectus at page 37 shows graphs of this statistic for the years 1993 to 2003 and says that the Australian market has grown by 1.7% p.a. compounding between these years.

We follow this up with a line graph showing the years 1990 to 2005 on the x axis and carprt quantity on the y axis. The first 40 million sq meters is not shown so the differences between years is exaggerated on the graph.

The series 1 line shows the same figures as the page 37 bar graph but with the years 1990 to 1992 added. Series 2 is the 1.7% compounding growth line derived by Feltex. This calculation takes only these two years into account. As can be seen 1993 was a very low year in terms of market size growth and 2003 was a high one. Series 3 is a projection of that same line from 2003 and Series 4 is the 1% compound growth line as apparently was used by Feltex for their projection of the company’s 2005 revenue.

Series 5 is the Microsof Excel forecast considering the data for the 10 most recent years 1994 to 2003. Feltex also claims to be considering the 10 most recent years. Note that this average line falls some 3% below actual figure for v2003. Series 6 indicates the adjustment that needed to be made to Feltex,s 2003 revenue to provide a realistic projection for 2005. This contrasts with Feltex’s unreasonable adjustment depicted by Series 4. Actual figures have to go below the average line as much as they go above it. The unreasonableness of Feltex’s projected revenue is close to 6%. They did not necessarily have to use the trend in recent market size figures to as the basis for projecting their 2005 revenue if they thought they had a better method. But they have indicated that this is what they did, and given so it had to be done properly.

We deplore the Securities Commission in for endorsing this fraudulent method of Feltex for projecting its 2005 revenue and also the National Government for leaving the Securities Commission in tact despite tinkering with or rearranging most pubic boards and commissions. Indeed the Commerce Minister has been completely irresponsible in appointing ex Feltex director Joan Withers to the board of Mighty River Power.

Series 5 is the Microsof Excel forecast considering the data for the 10 most recent years 1994 to 2003. Feltex also claims to be considering the 10 most recent years. Note that this average line falls some 3% below actual figure for v2003. Series 6 indicates the adjustment that needed to be made to Feltex,s 2003 revenue to provide a realistic projection for 2005. This contrasts with Feltex’s unreasonable adjustment depicted by Series 4. Actual figures have to go below the average line as much as they go above it. The unreasonableness of Feltex’s projected revenue is close to 6%. They did not necessarily have to use the trend in recent market size figures to as the basis for projecting their 2005 revenue if they thought they had a better method. But they have indicated that this is what they did, and given so it had to be done properly.

We deplore the Securities Commission in for endorsing this fraudulent method of Feltex for projecting its 2005 revenue and also the National Government for leaving the Securities Commission in tact despite tinkering with or rearranging most pubic boards and commissions. Indeed the Commerce Minister has been completely irresponsible in appointing ex Feltex director Joan Withers to the board of Mighty River Power.

Ms Withers joined the board apparently only some 10 day’s before the issue of the prospectus, allowed her photo to be used in the prospectus and signed the prospectus. We say this was all a very dangerous thing to do at short notice. And it would appear that she did not study the prospectus. The words on page 37 “In the period 1993 to 2003 … the compound average growth rate of the carpet has been 1.7% per annum” clearly implies that this is a fair measure of recent “growth” of the market as a basis for predicting what the changes in market size might be. But it could readily be seen from the graph that it was not that. Feltex took only the market size of two years into account and the earliest one, 1993, was so far from the present to be barely relevant. That is fraud because there was no other possible reason for publishing that part of the sentence other than to give readers a false impression of market growth. And why was there no graph or table of recent market share of the company when market share was a critical factor in its projections? There is no excuse for Ms Withers not picking up these matters and resigning as a director before the prospectus was issued. We cannot afford to have such gambling directors controlling our companies. Also Ms Withers action in resigning from Feltex when the going got tough was entirely unacceptable. We need to have directors who are prepared to stick with it and ensure that things are done legally and the best legal outcome is obtained for shareholders. We surmise that Ms Withers was encouraged to go into Feltex when she did and encouraged to get out of it when she did by someone who might widely be considered respectable such as the chairperson of the Securities Commission. But that is no excuse for Ms Withers. Directors must act independently. There is no excuse for Mr Powers bailing her out in this manner. Subscribers to the Feltex IPO are trying to sue her and she is undeserving of his support. Well actually her appointment is subject to “due diligence”. We don’t really know who is checking out who. Given the tight timing of her entry into Feltex we thought it would be Ms Withers now wishing to demonstrate how careful she now is but it could be the other way around. An appointment made at the same time to Meridian Energy was also subject to due diligence but that appointee now shows up on the Meridian web-site as a director. As at 14 July Ms Withers was not on the Mighty Power website although Mr Keith Smith the chairman of The Warehouse (where Ms Withers has also been a director in the past) was appointed to Mighty River at the same time and is on the site’s director list.

But Ms Withers is not the only player who has failed to pick up upon and react to the deceit in the Feltex prospectus by any means. Indeed in her case it might be a matter of gross neglect only. For most of the rest this failure is deliberate and a means by which successive governments have deceived the populous, ie abuse of accounting standards. These people come in two categories; those who should have detected and advised of the corruption at the time the Feltex IPO was issued or earlier, and those who had a duty to, or claimed to have, checked out the situation at a later date in the knowledge that something had gone horribly wrong with the company.

We wish concentrate on the latter category and go over various people and bodies who have chosen to ignore the blatant overstating of trends in market size in the Feltex prospectus and its failure to supply history of market share despite hinging it projections on these two concepts. .

Its hard to know where to start but let’s start with Bruce Sheppard and followers who have formed the NZ Shareholders Assn. Well they called a conference on Feltex some time ago and considered the possibi8lity of taking action on behalf of members and perhaps others who got caught out. They vowed not to have anything to do with the directors for five years, but we have not heard anything from them over this posting of Joan Withers to the board of Mighty River Power. Mr Sheppard seems to have changed tack doing almost a u-turn. He does not appear to back the action being taken by many shareholders to try to recover their funds. The association is probably not as big as it cracks itself up to be but it could easily publicly support the cause and vow to give as much assistance as it can to those taking the action even if the entrepreneur concerned, Tony Gavigan, has shut them out of the loop to protect his own commercial advantage. The Shareholder Association’s website has no recent references to Feltex, the most recent ones concern recruiting members and the need for issues like Feltex to create a membership surge. Well such issues might have continued to bring in members if the association had done anything for members taken in by Feltex i.e. if they had assisted them to get their money back or were trying their best to do so. It is no use just moving on to the next issue like a journalist. Some Feltex shareholders turned to the association thinking it might do something but but it did not do so. It would seem wrong to entice the victims of another such collapse by offering false hope. .

Mr Sheppard was very keen to get the Feltex into receivership. We think that as head of an organization with such a national name he was also influential in determining who the liquidators would be. But we suspect that he chose them because he knew that they would take minimal or no action. Mr Sheppard saw the Feltex director John Hagen, (appointed to replace Joan Withers as a useful “litigation accountant”. This site has never seen any merit in the work of Mr Hagen, the accounting expert in the case Hedley v Kiwi. We think Mr Sheppard for his own vested reasons does not want any action taken against (former) Feltex directors.

Next we have the liquidators of Feltex. Finnigan, Vague, and Whitfield are the names.

In order to get liquidation jobs no doubt one has got to undertake to meet the needs of those who are influential enough to put the business one’s way. This no doubt can create conflict with their legislative obligations and their professional obligations. In this case all three liquidators are members of the NZ Society of accountants. They claim to have done extensive work in investigating the Feltex IPO. We say that they have willfully failed to disclose that the page 37 reference to 1.7% compounding growth in market size is fraudulent as it can only be implied that that was a fair measure of recent growth in the market. Similarly with respect to market share it was improper for Feltex to assume a 1% increase for 2005 and not disclose what its recent experience had been in this respect. It was dropping at around 7% p.a.. The assumptions were not reasonable as required by the relevant Act. This foreseeable revenue drop is sufficient to account for Feltex’s entire profit drop in 2005.

In order to get liquidation jobs no doubt one has got to undertake to meet the needs of those who are influential enough to put the business one’s way. This no doubt can create conflict with their legislative obligations and their professional obligations. In this case all three liquidators are members of the NZ Society of accountants. They claim to have done extensive work in investigating the Feltex IPO. We say that they have willfully failed to disclose that the page 37 reference to 1.7% compounding growth in market size is fraudulent as it can only be implied that that was a fair measure of recent growth in the market. Similarly with respect to market share it was improper for Feltex to assume a 1% increase for 2005 and not disclose what its recent experience had been in this respect. It was dropping at around 7% p.a.. The assumptions were not reasonable as required by the relevant Act. This foreseeable revenue drop is sufficient to account for Feltex’s entire profit drop in 2005.

The liquidator’s cannot excuse their failure to disclose and act upon the above deceit on “respect” for the Securities Commission. Their job is to form their own objective view of the situation and take appropriate action.

A similar situation applies to the Securities Commission. But the case against them is more clear cut because they have made a few comments about the Feltex IPO. We do not wish to deplore the making of comments however. But comments must be reasonable and rational. We reject entirely the statement at paragraph 61 of the Commission’s 11 October 2007 statement on Feltex which says that the Commission found that most of Feltex’s assumptions presented a largely no change scenario. This statement is false. The Commission does set out the two critical assumptions being items (a) and (c) of paragraph 61. Item (a) is the 1% market growth assumption.

Item (c) the 1% increase in market share assumption compares with falls in market share of the 7% and 9% order occurring in the 2001-2003 period. Just who are these commissioners. Well it seems the general idea is to have equal numbers of lawyers, accountants, and company directors. But the number of commissioners is so large it is hard to hold anyone responsible for anything except perhaps the chairperson. The never say who did not take place in any decision because they have some personal interest so the public does not know what is going on. Why the personnel on this body has not been adjusted by the incoming Government we have no idea. More on these personnel here soon.

to top of pageAdvertising section

We link to: Accounting Page - Comprehensive Accounting Resources and Directory.Internet Web Directory - The internet's fastest growing directory of the best web sites. Fully searchable and updated regularly. We Advertise:

Books

Case studies of ICANZ coverups 2 Ernst and Young report to Dairy Co shareholders

Pokemon

Gifts

Cars

Toys

MP3

Videos

Dolls

Garden tools

Jewelry

------------------------

Structure and Operation of an alternative Accounting Organisation designed to shun dishonesty.

Suitable Objectives

Register of Members

Members Forum - Topical * open to all meantime: Plenty of Opinion

Magazine Plans

Need an Accountant? or Prepared to Change?

Users Forum * have your say

Ready to Join?Offering some Help?

Knowledge Tests * being developedInformation Bulletins

Why it is being Proposed

What's Wrong with the existing accounting body?

So called BNZ Auditan extensive case study Current Attitudes of Existing Institute

Visit our Advertising page from

Here